IME Twin-Engine Investment Framework

Stock selection driven by the 2 core drivers of long-term value creation: Earnings Growth & Change in Valuation Multiples

Understanding the Twin-Engine Investment Framework

We identify two primary drivers of value creation –

- Earnings Growth: The core driver of companies becoming larger & increasing value over a period of time

- Valuation Multiple Changes: Changes are driven by changes in growth outlook, fundamentals, sentiment & perception

We call this the “Twin Engine Framework”.

Our research focus is on a detailed assessment of how earnings and multiples are likely to change over time.

This provides a clear perspective on likely stock prices in the future & clarity on what drives changes in stock prices (business growth, multiple changes, or both).

The twin-engine framework helps build a strong quantitative rigour & discipline to stock selection.

Engine 1 - Earnings Growth

Engine 2 - Valuation Multiples

The twin-engine framework simplifes analysis of highly dynamic factors driving stock prices

Industry Trends

Industry outlook

Competitive dynamics

Pricing trends

Financials

Growth drivers

Margin outlook

Capital efficiency

Risks

Regulatory

Disruption

Competition

Quality

Accounting

Balance sheet strength

Barriers to entry

Management

Mgmt vision & execution

Corporate governance

Professionalisation

Catalysts/Triggers

Management change

Cyclical uptick

Restructuring

The twin-engine framework simplifies complex changes in diverse business fundamentals, into two quantifiable factors i.e. expected changes in growth & multiples.

This provides clear visibility into expected drivers of future stock price movements.

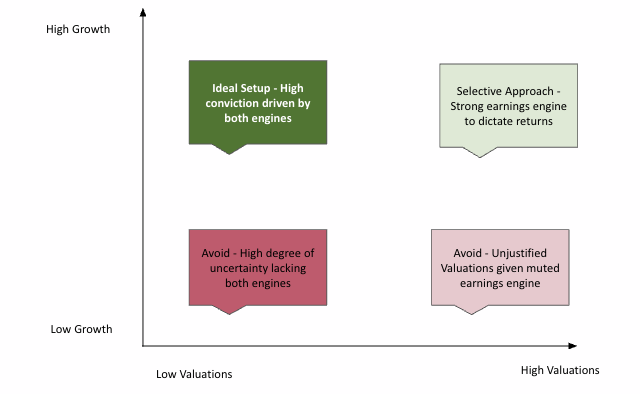

Understanding the segments we focus on

Our ideal companies are companies with high growth, that have the potential to re-rate. These can be hard to find, and are typically found by idenitifying sectors & companies where there is an underlying change in growth momentum or the quality of the business. Both the earnings growth & valuation multiple engines work in tandem to deliver strong outperformance in this quadrant.

We also invest in companies which we believe have high growth and are available at reasonable valuations. Here, stock price growth is driven by earnings growth, and not an increase in valuation multiples.